Only a few telecom products ever have been universally adopted by consumers. Voice, messaging, mobility, internet access and video entertainment are those products. Everything else is a niche. The paucity of universally-demanded services illustrates the problem of new service creation. It never has been easy, and will not be easy.

At the same time, it is easy to illustrate the new range of universally-demanded services, such as social networking, search and shopping, supplied as apps accessible “over the top,” and not intrinsically bundled with an access service.

Given the historic high demand for network-delivered content (video, especially), it comes as no surprise that OTT entertainment video services are so popular. As was the case for use of voice, new forms of highly-popular services (mobile voice rather than fixed) have much-higher value for consumers.

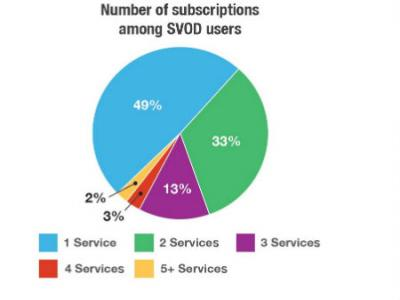

A majority of U.S. online consumers, for example, now subscribe to at least one paid OTT video service, according to researchers at IBB Consulting Group.

About 33 percent of those subscribers buy two services and 18 percent subscribe to three or more services.

Some 63 percent of paid OTT subscribers also subscribe to a linear TV service from their cable, telephone or satellite provider.

What is not yet clear is how demand for “live” events and programming will develop. Up to this point, the largest streaming services have offered pre-recorded content. Only recently have services that deliver “real time” programming begun to be widely available.

To the extent that all OTT video services involve bundles of some sort--either bundles of pre-recorded content or bundles of “live” channels--one major question for suppliers is the future shape of bundles (large or small numbers of networks, live or pre-recorded content, content genres).

The biggest questions concern channels that mostly rely on “live” content, as it is somewhat obvious that pre-recorded content is “best” or “easily” delivered using some on-demand format. News (for some) and sports (for more) provide the clearest examples of content venues especially leading the “live” category.

At least so far, buying behavior suggests that for “libraries of content,” a price of about $10 a month for an OTT service is viewed by consumers as reasonable. Since about 60 percent of consumers buy both linear and at least one OTT service, current propensity to buy represents something north of $90 a month in total spending.

The big issue for OTT is whether average spending ultimately is closer to $10 a month than $100 a month. Many of us would argue the eventual result is a blended average revenue per user close to $50 a month, including $40 a month for a skinny linear bundle, plus at least one OTT service at $10 a month.

What is not clear is whether video suppliers can dramatically change the perceived value proposition. If so, ARPU could stickier on the high side. What the subscription video industry hopes will result is that when a big bundle is purchased, all or most of that content also can be viewed on a streaming, over the top basis. That would tend to maintain current spending levels.

On the other hand, most consumers do not view most channels, creating constant pressure to craft more affordable, smaller bundles that meet the needs of most consumers.

What is not clear is whether video suppliers can dramatically change the perceived value proposition. If so, ARPU could stickier on the high side. What the subscription video industry hopes will result is that when a big bundle is purchased, all or most of that content also can be viewed on a streaming, over the top basis. That would tend to maintain current spending levels.

On the other hand, most consumers do not view most channels, creating constant pressure to craft more affordable, smaller bundles that meet the needs of most consumers.

No comments:

Post a Comment